Three Generations of Retirement Strategies

Generational disagreement is a constant of family life, but a recent survey found that millennials, Gen Xers, and baby boomers agree that saving and planning for retirement is a top financial goal.1

When it comes to pursuing that goal, however, each generation faces a different set of challenges. Of course, every individual is different, and there is no simple story for a whole generation. But here are some basic challenges and strategies to address them.

Millennials

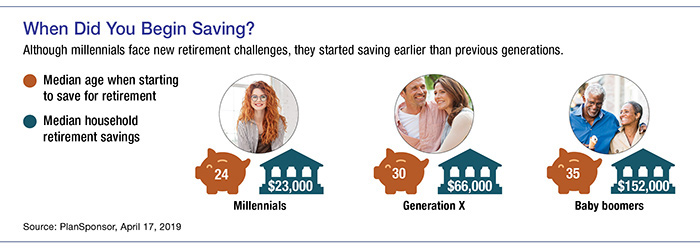

Many millennials entered the workforce during the Great Recession, which gave them a slow start in finding well-paying jobs. About two-thirds of millennials work for employers that offer workplace retirement plans — similar to other generations — but only a third actually contribute to a plan. Many are ineligible to participate in their employer’s plan because they work part-time or don’t have enough tenure.2 Millennials often carry high student loan debt, and they are most likely to feel the long-term effects of any reductions in future Social Security benefits.

The good news is that millennials are the most educated generation in U.S. history, and they have the most time to save. More than 94% of millennials who are eligible for a workplace plan participate. On average, they contribute 5% of their salaries (10% with an employer match). Experts recommend that workers contribute at least 15%, but millennials may need to save even more due to longer life spans.3 The fundamental strategy for this generation is to save as much as possible as early as possible, whether in a workplace plan, an IRA, or another savings vehicle.

Generation X

Gen Xers were just hitting the prime of their working years when the housing bubble burst and the financial crisis hit the markets, reducing their home values and investment portfolios. These assets have mostly recovered, but this generation often faces the challenge of saving for retirement while supporting younger children at home, paying for college for older children, and/or helping aging parents.

Like millennials, Gen Xers still have time to save, but their timeline is tighter, so it’s important to start looking at concrete numbers: analyzing current net worth and income, projecting retirement needs, and establishing a budget to meet those needs. This may involve a combination of simple adjustments (such as eating out less) and difficult choices (such as sending a child to a state college instead of a private school).

Baby Boomers

Almost half of baby boomers are already retired, and retirement is approaching quickly for those who are still working. Although this generation had the advantage of working during long periods of economic expansion that should have helped boost earnings and savings, many are woefully unprepared, due in part to the decline of pensions in private industry during their careers. One survey found that 45% of baby boomers have no retirement savings. Many boomers underestimate the income they will need in retirement as well as the cost of medical expenses and long-term care.4

Working boomers should have a written financial plan for retirement that includes expected sources of income and projected expenses. If expenses exceed income, there may be time to accelerate savings enough to meet projected needs. Boomers (and older Gen Xers) can take advantage of catch-up contributions (for those age 50 and older) to workplace plans and IRAs. Some may have to work longer and/or cut back on their anticipated retirement lifestyle.

Saving for retirement is a long road with many twists and turns along the way. Whatever your generation or personal situation, it’s better to address the challenges now rather than be surprised when you retire.

1) Business Insider, August 21, 2019

2–3) National Institute on Retirement Security, 2018

4) Insured Retirement Institute, 2019

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2020 Broadridge Investor Communication Solutions, Inc.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today.