Three Lessons from Retirees

Each year, the Employee Benefit Research Institute (EBRI) surveys workers and retirees to assess how confident they are in their ability to live comfortably throughout retirement. In 2019, only 67% of workers reported feeling “very” or “somewhat” confident, compared with 82% of retirees.1

A closer look at the survey results reveals important lessons to be learned from retirees, whether your own retirement is coming soon or a distant goal.

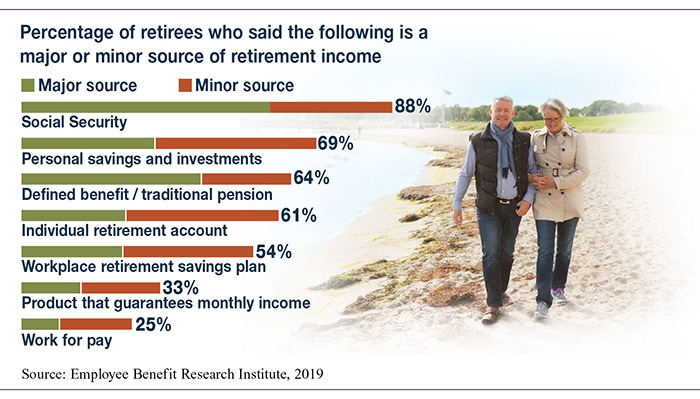

Lesson 1: Don’t count on working longer. Almost three out of four workers expect work-related earnings to be at least a minor source of income in retirement, but just one in four retirees has worked for pay.2

Moreover, there is typically a big gap between expected and actual retirement ages. In 2019, workers expected to retire at a median age of 65, whereas retirees actually retired at a median age of 62. More than four in 10 retirees retired earlier than planned, often due to health issues or changes in their work situations.3 Your target retirement age is one area where you may want to hope for the best but prepare for the worst.

Lesson 2: Your income will largely depend on your savings efforts. Even though 64% of retirees receive income from a defined benefit plan (traditional pension), an even larger percentage rely on savings and investments, and more than half rely on income from IRAs and/or workplace retirement plans. Current workers are much less likely to have a pension, and more than half expect employer plans to play a “major” role in their retirement funding.4

If you have access to an employer plan, focus on saving as much as possible — and don’t despair if you are close to retirement and far behind your savings goals. You might be surprised by how much progress you could make in a few years. In 2020, you can contribute $19,500 to a 401(k) or 403(b) plan and an additional $6,500 catch-up contribution if you are age 50 or older.

Lesson 3: Health care may cost more than you think. More than one out of three retirees said their health-care or dental expenses were higher than they anticipated.5 Be sure to include medical expenses in your retirement savings strategy. According to another annual EBRI report, a 65-year-old couple who retired in 2019 might need about $300,000 to pay health-care expenses in retirement.6

1–6) Employee Benefit Research Institute, 2019

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2020 Broadridge Investor Communication Solutions, Inc.share|

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today.