Annuity Strategies: Living Benefits Can Help Counter Retirement Risks

An annuity is an insurance contract that offers an income stream in return for one or more premium payments. Income payments continue for the duration of the contract, which may be for life or a specific number of years.

A fixed annuity offers a set rate of return for the life of the contract. A variable annuity is riskier but offers the potential for growth because a portion of the premium is invested in the financial markets; the annuity’s future value and income payments are largely determined by the performance of the investment subaccounts selected by the account owner.

Guaranteed living benefits are optional riders that can be attached to annuities for an additional cost. Here’s how living benefits might help you address two important retirement risks.

1. Outliving Your Savings

You can receive a lifetime income stream from an annuity in one of two ways: annuitization or withdrawals. When a contract is annuitized, the cash value is converted into a series of periodic income payments based primarily on current interest rates (or market-based returns) and your life expectancy. Control of the account transfers to the insurance company, so you no longer have access to the investment principal.

A guaranteed lifetime withdrawal benefit (GLWB) is an optional lifetime income rider that can be attached to a variable annuity. It guarantees that you can withdraw a minimum amount of income from a variable annuity for life without having to annuitize, even if the original account value is depleted. If the markets perform well, the income amount could increase, but it typically cannot decrease unless you take a withdrawal that exceeds the guaranteed withdrawal amount. The remaining account value may be available for other purposes and inherited by your designated beneficiaries after death.

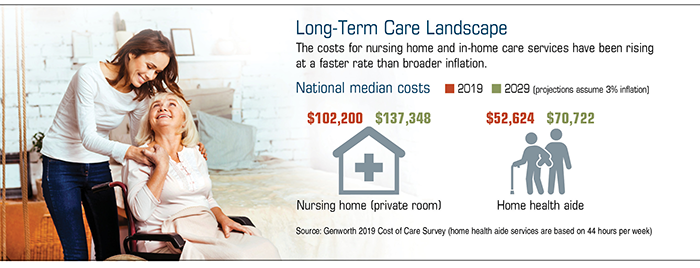

2. Paying for Long-Term Care

Adding a long-term care (LTC) rider to a fixed or variable annuity might help prevent your savings from being depleted by escalating costs. Benefits are typically triggered if you are diagnosed with dementia or are unable to perform two or more activities of daily living such as eating, bathing, and dressing. If care is needed, the payout is increased for a specified period of time or until the account value reaches zero. And if you never need care, you can continue to earn a return on your money. Medical underwriting requirements tend to be more lenient with an LTC rider than with a standalone policy, and you don’t have to worry about future rate increases or the issuer canceling the policy.

Any annuity guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company. Annuities are not guaranteed by the FDIC or any other government agency. They are not deposits of, nor are they guaranteed or endorsed by, any bank or savings association. Annuities typically have contract limitations, fees, and charges, which can include mortality and expense charges, account fees, investment management fees, administrative fees, charges for optional benefits, holding periods, termination provisions, and terms for keeping the contract in force.

A variable annuity is a long-term investment product designed for retirement purposes. Variable annuities that come with living benefits tend to have more limited investment options. The investment return and principal value of the investment options are not guaranteed and may fluctuate with changes in market conditions. When the annuity is surrendered or annuitized, the principal may be worth more or less than the original amount invested.

Variable annuities are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the variable annuity contract and the underlying investment options, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2020 Broadridge Investor Communication Solutions, Inc.

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today.