Municipal Bonds

Municipal bonds are issued by public entities such as state and local governments, health systems, universities, and school districts to help finance ongoing expenses and major projects such as roads, water systems, and facilities. An attractive feature of these bonds is that the interest is generally exempt from federal income tax, as well as from state and local taxes if you live in the state where the bond was issued.

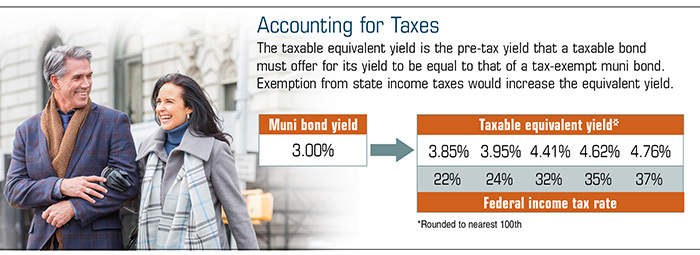

For this reason, muni bonds and funds have long been a mainstay in the portfolios of income-focused investors who want to manage their tax burdens. The tax-free yields are often more valuable to investors in higher tax brackets.

The 2017 Tax Cuts and Jobs Act introduced changes to tax rates and allowed deductions that impact some investors more than others, with implications that spill into the municipal bond market.

An Altered Landscape

If an investor’s new marginal tax rate is much lower than before, the tax exemption might also be less valuable. However, the federal deduction for state and local taxes (SALT) is now limited to $10,000 a year. For many affluent investors in high-cost, high-tax states such as New York, New Jersey, California, and Connecticut (among others), the appeal of tax-free income is stronger than ever. Consequently, a surge in investor demand drove up muni bond prices and pushed down yields in 2019.1

Another tax provision made income from some municipal bonds (“private activity” bonds that often fund stadiums and airports) subject to the federal alternative minimum tax (AMT). The AMT is a parallel tax system with different rates and rules that disallow certain deductions. Fortunately, the phaseout threshold for the AMT also increased (from $160,900 in 2017 to $1,020,600 in 2019 and $1,036,800 in 2020 for joint filers), so many households no longer need to worry about the AMT.

Tax-Exempt Funds

Some muni bond funds and exchange-traded funds (ETFs) are national and offer income free of federal income tax, but they may be subject to state and local taxes. Other funds focus on bonds from one specific state and may also include bonds from U.S. territories that are not subject to state taxes, making the fund’s interest income tax-free for investors who live in the targeted state.

Investors should keep in mind that capital gains taxes could still be triggered if tax-exempt bonds or fund shares are sold for a profit. Also, tax-exempt interest is included in determining whether a portion of any Social Security benefit received is taxable.

Review the Risks

Because government entities have the power to raise taxes and fees as needed to pay the interest, muni bonds are generally less risky than corporate bonds. The 10-year default rate for U.S. investment-grade municipal bonds is 0.18%, compared with 1.74% for investment-grade corporate bonds.2

Regional economies and the financial strength of issuers can vary widely, so municipal issues are rated for credit risk, as are other bonds. A credit rating ranging from AAA down to BBB (or Baa) is considered “investment grade”; lower-rated or “junk” bonds carry greater risk.

As interest rates rise, bond prices fall, and vice versa. When redeemed, bonds may be worth more or less than their original cost. Bond funds are subject to the same inflation, interest-rate, and credit risks associated with their underlying bonds. The return and principal value of bonds and mutual fund shares fluctuate with changes in interest rates and other market conditions, which can adversely affect investment performance.

Mutual funds and ETFs are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

1) The Wall Street Journal, August 7, 2019

2) Municipal Securities Rulemaking Board, 2019

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2020 Broadridge Investor Communication Solutions, Inc.share|

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today.